| Address: Mumbai City, Maharashtra, 400001 |

| Website: cibil harrassment |

Understanding a settlement and waived off settlement given by Private banks to its Borrowers - loan defaulters:

There is an important need to understand the legal differance between the two.

A settlement is done by a bank when it understands that a loan consumer is unable to pay the loan availed by him / her .

For ex: a person avails 1 lakh as a loan and has been paying the installment regulary and due to circumstance - the loan defaulter is deemed as a circumstantial defaulter.

Thus the lending bank provides an option to the loan defaulter to arrive on a onetime setllement.

How does a onetime settlement work:

if a person who borrowed 1lakh pays the bank 50 thousad the bank looses net to net of Rs.50, 000 on their BALANCE SHEET -Book of AUDITS Banking Records.

The same will be claimed by the BANK at the end of the Financial Year as loss to the RBI to claim Credit Leniency and allowance benefit of RBI to be given to the particular bank to cover up a certain part of the loss of 50 thousand.

Now if the RBI accepts this claim of the bank and gives 20, 000 as a credit allowance the bank will cover up certain loss of 50, 000 and the loss for the bank will be minimised to 30, 000.

However for the client or herin the borrower -loan defaulter he remains a defaulter permanently for life as the RBI lost 20, 000 for his shortcoming to pay the bank.

This causes the CREDIT Information Report of the Loan defaulter permanently marred and he will not be entittled to avail any loan in future from any bank.

Waived of SETTLEMENT:

The borrower who is unable to repay the bank a loan, himself authorises a banking legal counsel to address his greviance with the bank, writes to the bank that he is unable to repay the bank.

Also the borrower can only legally register his case of default- subject to arbitratory resolution : through an RBI authorised legal counsel will 1st register the matter with the banking council and then legally explain to the bank and its legal departement that whatever amount paid by the borrower as installment got adjusted to high interest rate imposed by the bank which was untold, not properly explained to the borrower and this is the principle reason that he is presently in such a situation that he isnt able to pay anymore unless the bank arrives on a mutually agreeable and logical solution. This is a case of irregularity in interest rates. The banks also take such matters quite seriosuly as it will be an offence on the bankers part under wrongfull raising of bills under debit of charges.

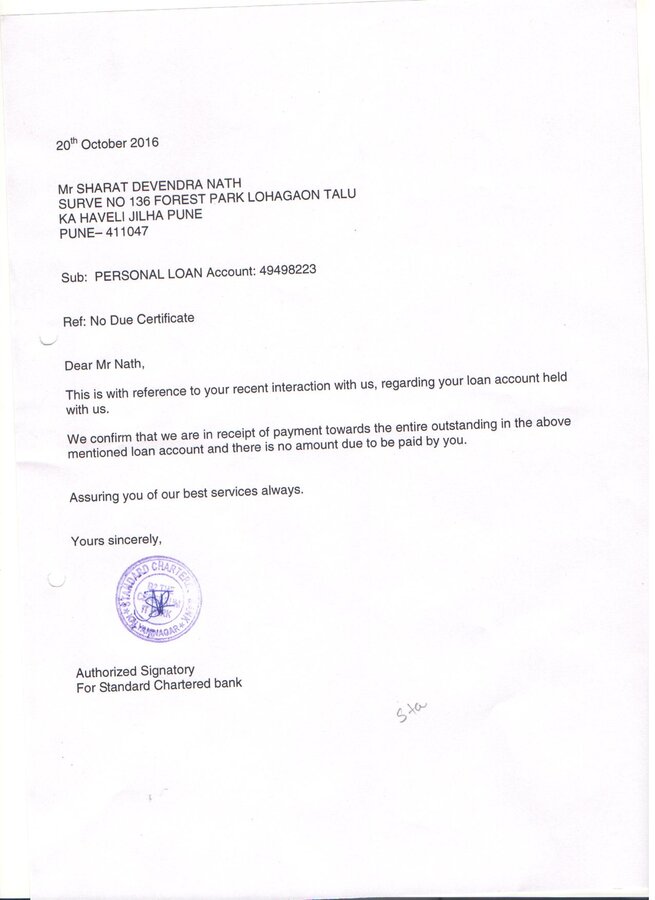

On achieving an agreed resolution the borrower shall agree to pay the amount agreed upon and the bank inturn will give a no objection letter -waived off cum settlement letter.

The waived off- NOC letter will releave a loan -borrower from entire liability from the bank and all banking bodies.

On achieving the waived off noc letter the CIR Report of the borrower is cleared. Thus the borrower can avail loans from any bank.

This process is called arbitration - adjudicatory resolution and takes 5 working days for completion.

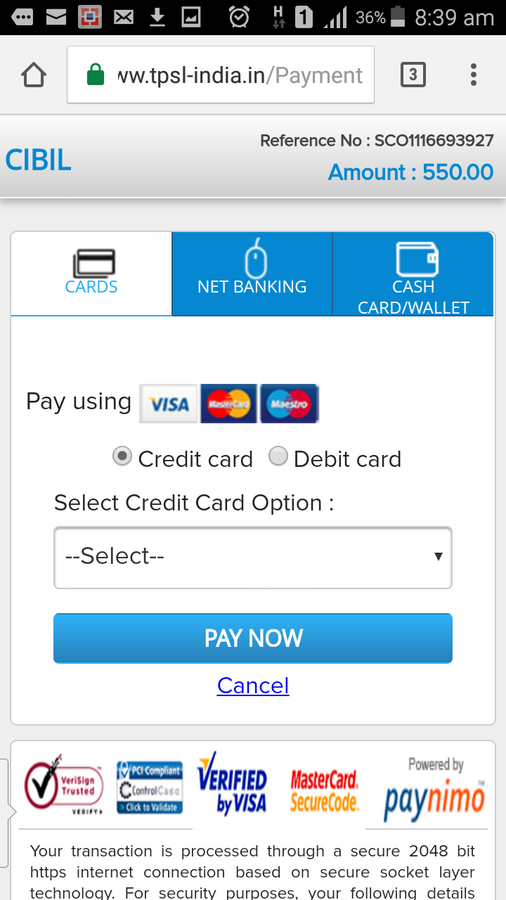

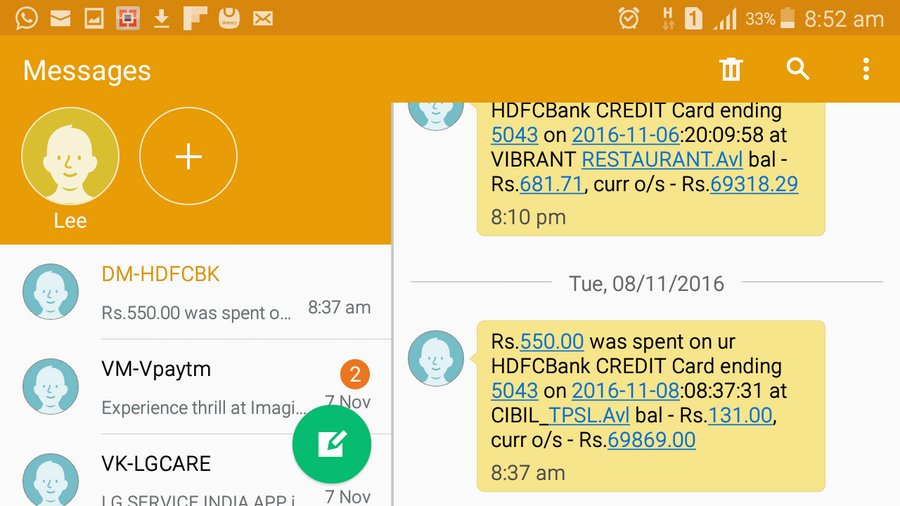

CONSUMERS : This is an Informative provided me who has suffered from CIBIL even inspite of making one time settlement. Studied the above rules. Please donot fall prey to calls or whatsapp messages forcing to make one time settlements .This is a trap of recovery agents or telecallers employed by banks.

Before making any payment based on phone threats or mobile or whatsapp threats kindly contact Mr. Ebenezer at [protected] for advice . Mr.Ebenezer is a Banking legal expert and a cyber law expert.

Jan 26, 2017

Complaint marked as Resolved Credit Information Bureau India [CIBIL] customer support has been notified about the posted complaint.

Dec 24, 2016

Updated by E B Soans India Display of data by CIBIL on a one sided baised data is Illegal and amounts to wrongful display of public data which is a cyber crime. In recent times bank recovery agents also threaten consumers in name of CIBIL vide whatsapp messages. All these are cyber crimes and this is because banks have given undue importance to These are technolegal issues which need to be addressed by professional banking legal advocates. One of the oldest cyber legal expert dealing with financial and technolegal crimes related to banking is Mr. Ebenezer Nathaniel . You can contact him at [protected]. He has a PAN India Service.

I had faced similiar problems and was getting blackmailed by recovery agents and bank officials threatening to post wrong displays in CIBIL unless until I pay extra payment of Rs.20, 000 other than my actual dues. CIBIL has become a principle blackmailing medium for these recovery goons and banks.I approached Mr.Ebenezer Nathaniel and all my worries were squashed out legally in just a week. My cibil is displayed correctly now and I paid only the actual dues to the lender bank. Thus if you have any problems and issues regarding CIBIL I strongly recommend you to approach Mr.Ebenezer Nathaniel and successfully resolve your issue immediately.

Verified Support

Dec 26, 2016

Credit Information Bureau India [CIBIL] Customer Care's response Dear E B Soans,

Please write to us at [protected]@cibil.com

Regards,

Team CIBIL.

![Credit Information Bureau India [CIBIL] Logo](/thumb.php?bname=1&src=cibil.jpg&wmax=280&hmax=280&quality=90&nocrop=1 "Credit Information Bureau India [CIBIL] Logo")

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Request you to raise your complete issue at [protected]@hdfcbank.com along with your issue details, registered contact details, account and branch details. with ref ID-TTU[protected] in the subject line. Will get back to u. -Anay